News

.png)

Eric Ries, chairman of the Long-Term Stock Exchange, spoke to the Wall Street Journal on what it takes to foster socially responsible investing.

Eric Ries, chairman of the Long-Term Stock Exchange, spoke to the Wall Street Journal on what it takes to foster socially responsible investing.

Wall Street Journal

Wall Street Journal

'Lean Startup' guru Eric Ries just launched a new stock exchange that values companies based on principles like employee wellbeing, diversity, and inclusion. Take a look at how it works.

'Lean Startup' guru Eric Ries just launched a new stock exchange that values companies based on principles like employee wellbeing, diversity, and inclusion. Take a look at how it works.

Marguerite Ward, Insider

Marguerite Ward, Insider

People laughed at startup guru Eric Ries' idea to reinvent Wall Street, so he started a new stock exchange to prove them wrong

People laughed at startup guru Eric Ries' idea to reinvent Wall Street, so he started a new stock exchange to prove them wrong

Becky Peterson, Business Insider

Becky Peterson, Business Insider

Silicon Valley Vs. Wall Street: Can the New Long-Term Stock Exchange Disrupt Capitalism?

Silicon Valley Vs. Wall Street: Can the New Long-Term Stock Exchange Disrupt Capitalism?

Alexander Osipovich and Dennis K. Berman, The Wall Street Journal

Alexander Osipovich and Dennis K. Berman, The Wall Street Journal

.svg)

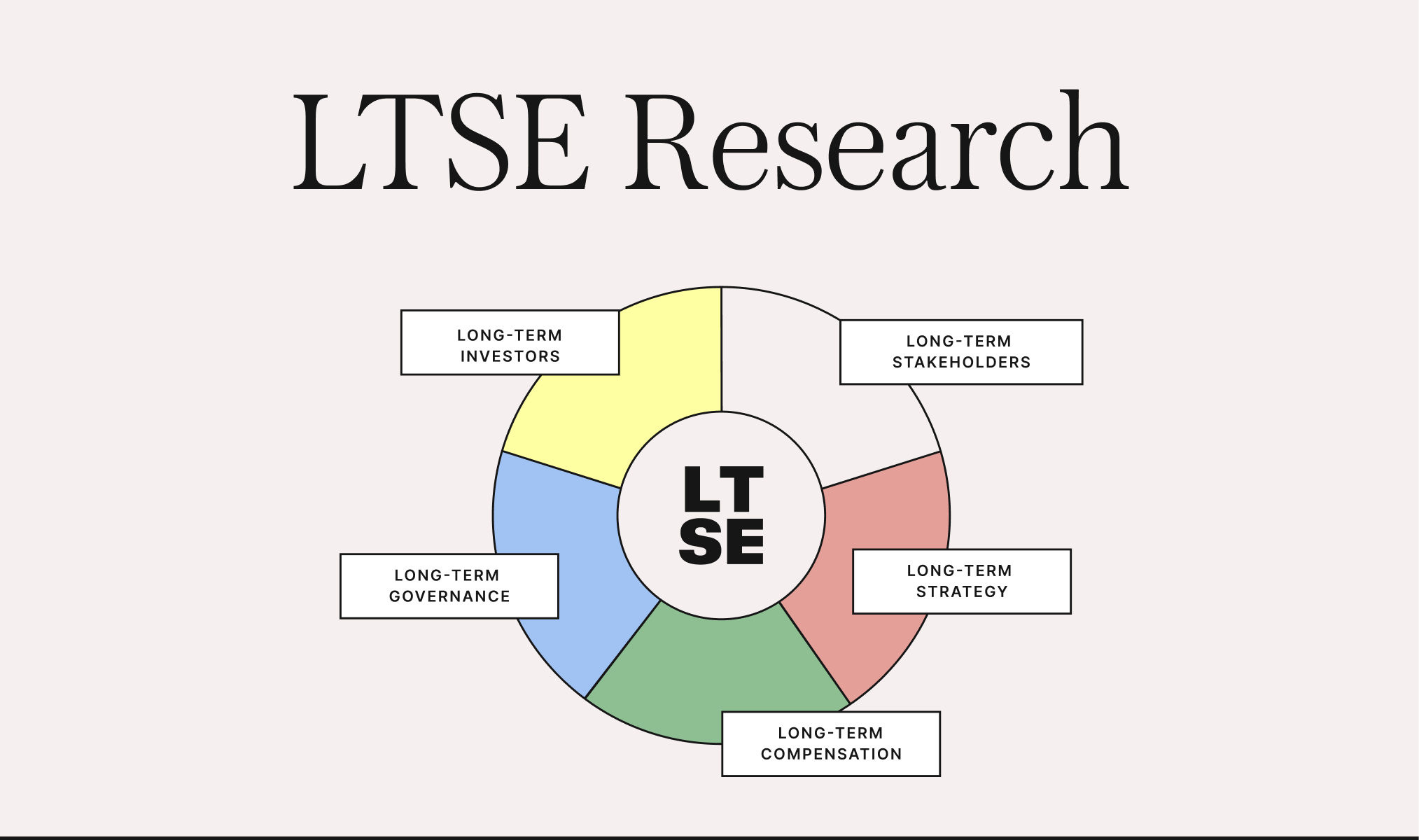

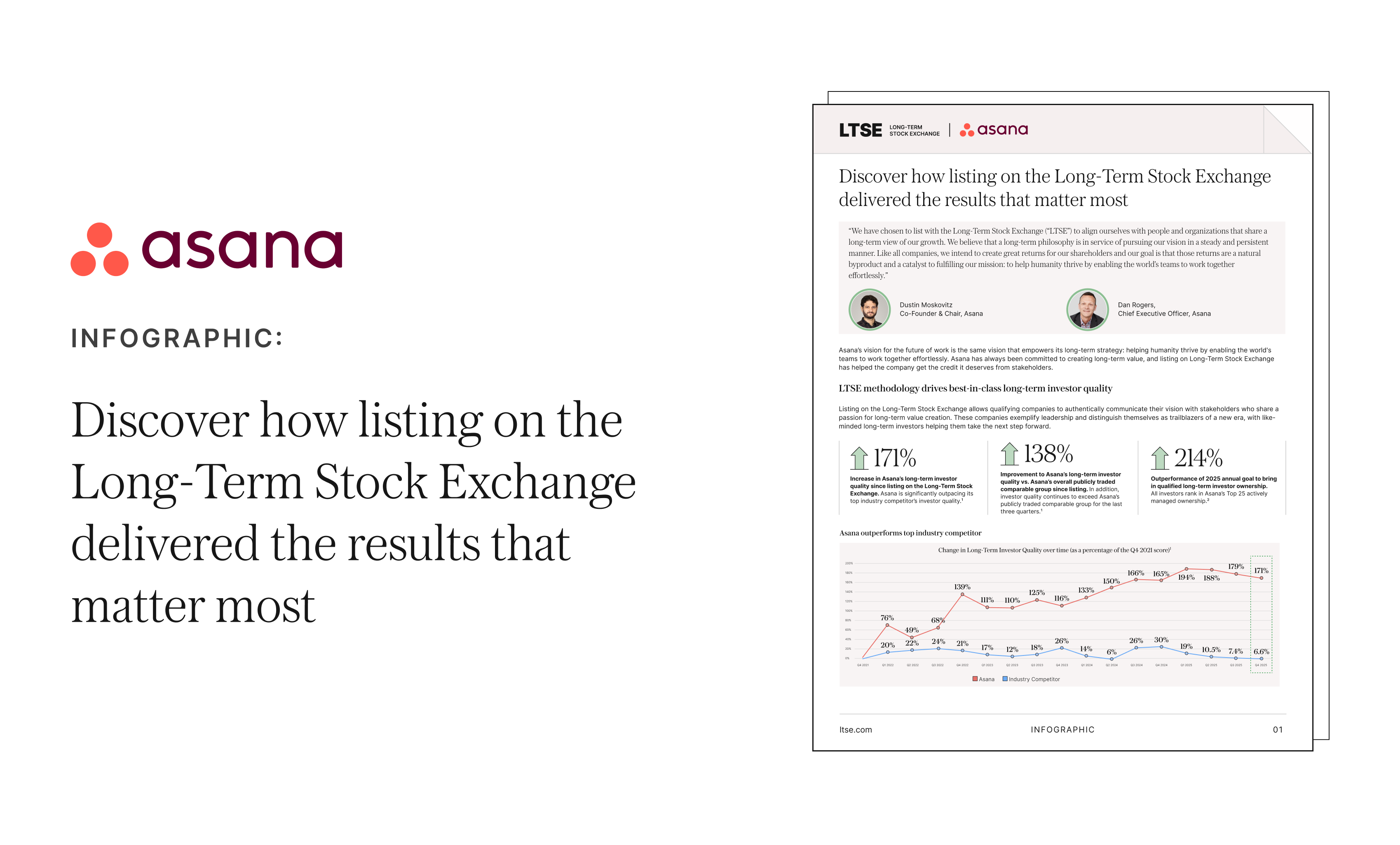

Public Company and Investor Insights

%20(1).png)

.svg)

Private Company and Investor Insights

.png)